Pastry and Bakery Ingredients Market Report 2025

As of November 2025, the pastry and bakery ingredients sector continues to navigate a complex interplay of commodity volatility, shifting consumer preferences, supply chain constraints, and innovation in alternative and functional ingredients. Compared to the January 2025 baseline, several ingredient categories have experienced more pronounced swings in pricing, margins, and growth prospects.

According to Mordor Intelligence, the global bakery and baking ingredients market is valued at approximately USD 21.29 billion in 2025. The sector is projected to grow steadily at a CAGR of 6.01%, reaching approximately USD 28.5 billion by 2030. Strong demand for high-quality ingredients is driven by evolving consumer preferences, product innovation, and expanding bakery applications. The consistent upward trend highlights the market’s long-term growth potential. Manufacturers and suppliers must remain agile, invest in innovation, and respond proactively to emerging industry needs.

The following section summarizes seven key ingredient categories shaping the global bakery and pastry market. It outlines the latest developments and key industry insights.

Cocoa Market Trends – Price Surge, Supply Challenges, and Growing Demand for High-Quality Beans

In January 2025, cocoa prices reached historic highs of approximately USD 10.75 per kilogram, one of the highest levels in six decades. Since mid-2025, prices have eased due to better weather, larger harvests, and reduced drought concerns in West Africa, which alleviated supply pressures. As of October 1, 2025, cocoa traded at about USD 6,683 per metric ton, around 20.7% lower than at the start of the year. New York cocoa futures had peaked above USD 8,000 per ton but later fell about 12%, settling near USD 6,936 in mid-September.

In Ghana, the Cocoa Board raised the producer price to GHS 58,000 per metric ton, around USD 4,628. This represents a 12% increase from previous levels. Nigeria will produce about 11% less cocoa in the 2025/26 crop. Ecuador is aggressively expanding production and could surpass competitors to become the world’s second-largest cocoa producer by 2026/27.

Implications for Pastry & Bakery Ingredients

The extreme price volatility witnessed earlier in 2025 forced major chocolate ingredient producers such as Barry Callebaut and Mondelez to either cut volumes or absorb narrower margins. Although prices have cooled from record highs, they remain significantly elevated compared to pre-2022 norms. For pastry and bakery ingredient formulators, this environment necessitates the use of forward contracting, hedging, and diversified sourcing strategies to manage ongoing risk. Premium and single-origin cocoa varieties continue to command strong price premiums, and the risk of renewed weather or pest-related disruptions remains high.

Forecast: Cocoa prices should stabilize slightly in the second half of 2025 as production improves. However, supply chain pressures will continue to drive higher prices for high-quality cocoa beans.

Source: ICCO – Barry Callebaut – Mondelez– Towards FnB

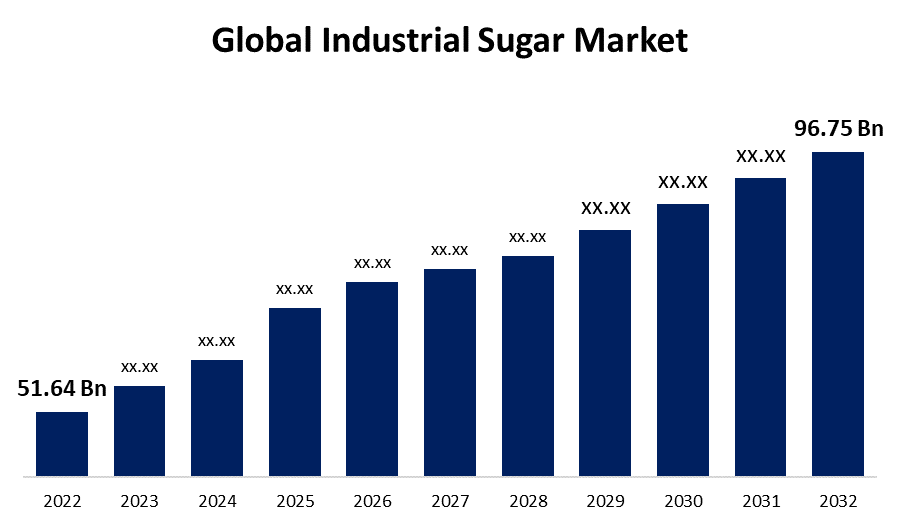

Sugar and Sweeteners Market Trends

How Sugar Markets Are Holding Up to Supply and Demand Shifts

The global sugar market remains more stable than cocoa, though cost pressures from logistics and energy persist. Demand for low-calorie, free-from, and clean-label formulations continues to increase across bakery applications. Higher production in China, India, and Thailand should offset potential shortfalls in Brazil. However, weather conditions and shifting trade policies could still create market volatility.

Although raw sugar prices have not experienced dramatic swings, input inflation and rising freight costs continue to erode margins. At the same time, high-intensity sweeteners such as stevia, monk fruit, erythritol, and allulose are gaining traction, driven by consumer demand for natural, lower-calorie alternatives. However, increased regulatory scrutiny surrounding non-nutritive sweeteners and labeling requirements could pose new challenges for suppliers.

Sugar prices should remain relatively steady over the next year, assuming no major weather events or trade disruptions occur. Growth in sugar alternatives will likely outpace traditional sugar usage in bakery applications, especially in developed markets where clean-label innovation is accelerating.

Source: USDA – Sugar and Sweeteners Market Outlook, AIFI, Spherical Insights

Fruit Ingredient Market Trends – Global Growth and Key Challenges

Global Fruit Ingredient Market & Crop Highlights

The global fruit ingredient market remains dynamic in late 2025, fueled by strong demand for clean-label, minimally processed, and plant-based ingredients. Brazil’s orange juice exports fell nearly 20% in volume in early 2024/25, but revenues rose 42.7% due to higher global prices. Global fruit production should grow from 934 million metric tons in 2023 to nearly 998 million tons by 2028, driven by fruit-ingredient demand. In the U.S., the fruit ingredients market reached about USD 56.8 billion in 2023 and is projected to grow at a 5.3% CAGR through 2030.

Market Dynamics & Supply Pressures

Berry markets remain strong, though not without challenges. Chinese strawberries faced early-harvest declines, pushing prices higher even as exports to Southeast Asia expanded. Mexican blueberries and raspberries continue performing well, supported by improved yields and pest-resistant varieties. Cold-chain logistics and freight costs remain major considerations, especially for tropical and off-season fruits. Seasonal weather variability, including heatwaves and irregular rainfall, continues to disrupt supply across berries, tropical concentrates, and other crops.

Cherry Crop Spotlight

Global cherry production is projected to decline more than 10% in 2025/26 to about 4.6 million tons. Smaller crops in Turkey, the EU, and the U.S. are driving this drop. Severe weather in Michigan has slashed U.S. production by 70%, while European crops are too limited to export. Chile plans to increase exports by nearly 10%, but overall supply tightening is pushing prices higher. Both fresh cherries and processed cherry ingredients are now more expensive, affecting bakery and pastry formulations. Companies source cherries almost exclusively from the U.S., and costs have risen sharply amid strong customer demand.

Consumer Trends & Product Innovation

Consumer demand is shifting toward clean-label, minimally processed fruit ingredients. Growing interest in gluten-free, plant-based, and reduced-sugar products is driving sector innovation. This includes exotic fruit blends, new purée varieties, and functional concentrates for bakery, snack, and beverage applications. Companies are also developing value-added ingredient formats optimized for off-season supply

Implications for Bakery & Pastry Ingredients

For bakery and pastry manufacturers, supply tightness; particularly for cherry-based and exotic fruit ingredients is creating upward price pressure due to crop shortfalls and logistics costs, yet this also presents an opportunity for companies investing in local sourcing, cold-chain efficiency, and flexible ingredient systems to achieve stronger margins and more reliable supply. Despite ongoing volatility, overall fruit-ingredient demand continues to rise, especially in emerging markets across Asia, Africa, and Latin America.

Source: Reuters – Brazil’s Orange Juice Exports – USDA Economic Research Service – Grand View Research

Fats and Oils Market Growth: Rising Demand for Healthier and Sustainable Oils

The global fats and oils market should grow from approximately USD 182.9 billion in 2024 to around USD 196.6 billion in 2025, sustaining a strong growth rate of 7.5–8.9% through 2028. Within the bakery sector, oils and fats remain a critical component for texture, structure, and flavor.

Prices for edible oils, including palm, sunflower, and canola, continue to face upward pressure from supply constraints, energy costs, and geopolitical uncertainties. Drought conditions in Eastern Europe and South America have further restricted output. At the same time, formulators are exploring healthier and more sustainable lipid systems, such as oleogels (liquid oils structured to mimic solid fats), interesterified oils (oils with rearranged fatty acids to improve stability and health profile), and structured lipids (fats engineered at the molecular level for targeted functional and nutritional benefits), which reduce saturated fat content while maintaining functionality. Sustainability and traceability have become essential purchase criteria for buyers, with deforestation-free sourcing now a standard requirement.

Plant-based, functional, and sustainable fat systems will continue driving the next phase of the bakery sector. Suppliers that adopt lower-carbon production and green processing technologies will gain a competitive advantage, although price volatility will persist amid ongoing global uncertainties.

Source: The Business Research Company – Fats and Oils Market Report

Dairy Market Trends: Recovery and Growth in Key Sectors

The global dairy market is currently facing seasonal weakness, with dairy derivatives showing a broad decline. This slowdown is primarily due to a reduction in demand as industrial users complete their holiday season operations. Weaker interest in milk powders was evident during the Global Dairy Trade (GDT) Pulse event, further impacted by the outlook for increased milk production in the upcoming calendar year. All major dairy exporting regions are forecasting favorable conditions, contributing to a more balanced supply and further dampening short-term demand.

In addition, milk prices have seen a significant increase since the beginning of 2025, rising by 1.69 USD/CWT, or 9.03%, according to trading on a contract for difference (CFD) that tracks the benchmark market for this commodity. Historically, milk prices reached an all-time high of 25.20 USD/CWT in May 2022. This uptick in milk prices, alongside the seasonal dip in dairy demand, adds complexity to the market dynamics.

Improved weather and feed supply have supported better milk yields in some regions, though energy and feed costs remain elevated. Demand for specialty dairy products such as lactose-free, A2, grass-fed, and organic variants continues to grow, reflecting consumer preference for premium and differentiated products. Plant-based dairy alternatives derived from oats, peas, soy, and almonds are also gaining traction in bakery applications, providing novel textural and emulsification benefits but requiring technical adjustments.

Forecast: The dairy ingredient market is likely to regain momentum as global demand for premium dairy products strengthens. However, plant-based dairy analogs will continue to capture market share, particularly in clean-label and allergen-free bakery formulations. Hybrid systems combining dairy with plant proteins are expected to become increasingly common.

Source: The Bullvine – Dairy Outlook – Global Dairy Trade (GDT) – USDA – Euromonitor International

Flour and Starch Market: Growth Driven by Demand for Gluten-Free and Plant-Based Products

The global flour and starch market is forecasted to grow at a CAGR of about 4.2 percent in 2025, reaching approximately USD 300 billion. The U.S. winter wheat acreage has expanded slightly to offset declining long-term production trends.

Regional disparities in harvest conditions continue to affect wheat and starch availability. Demand for specialty flours such as gluten-free, ancient grain, and high-fiber blends remains strong as consumers seek variety and nutrition. Functional starches like resistant or enzyme-treated starches are being adopted to improve product texture, shelf life, and nutritional content. Trade policies, export restrictions, and freight challenges remain potential disruptors of supply and price stability.

Flour and starch will continue to form the backbone of bakery formulations, but growth will increasingly favor innovation and value-added derivatives. Companies with vertically integrated supply chains from farming to R&D are expected to benefit from stronger margin control and consistent quality.

Sources: USDA Economic Research Service, Euromonitor International, Finance Yahoo

Egg Market: Global Growth and Key Challenges

U.S. Egg Production and Supply Challenges

In the United States, the egg sector continues to face considerable upheaval in 2025. According to the USDA Economic Research Service, production is projected to increase slightly on the layer‑inventory front, but overall supply remains constrained relative to pre‑crisis levels. As of September 1, 2025, the U.S. non‑organic commercial cage‑free table egg flock stood at 116.6 million layers (38.7% of the total table‑egg flock), up 9% year‑on‑year but still below historical peaks. Meanwhile, highly pathogenic avian influenza (HPAI) has led to the culling of an estimated 41.6 million hens across conventional and cage‑free systems, further straining supply.

Price and Trade Dynamics

Supply disruptions drove wholesale shell‑egg prices to historical highs earlier this year. Some price softness is emerging as production begins to recover. The U.S. remains mostly self-sufficient in shell eggs, but bulk egg-product exports and imports have grown in importance. Fluctuating domestic availability continues to influence trade activity.

Consumer Trends and Production Shifts

Consumer preferences continue to shift toward cage‑free and organic systems, driven by animal-welfare concerns, retailer commitments, and regulatory pressures. As of early 2025, about 42.1% of the U.S. table‑egg flock was in cage‑free or organic systems. These production-system changes involve additional costs; housing conversions, feed adjustments, and bio-security upgrades; that influence pricing and margin dynamics across the supply chain.

Despite these headwinds, the global egg market is projected to grow moderately. A recent industry study estimates a 10‑year CAGR of about 2%, totaling roughly 22% growth by 2032. Most expansion is expected in emerging markets across Asia, Africa, and Latin America. Rising incomes, urbanization, and evolving dietary preferences for affordable, high-quality protein are driving this growth.

Source: Eggs Unlimited Data – USDA Agricultural Marketing Service, Euromonitor International, and Fred

Summary of the Bakery Industry’s Trends and Consumer Behavior

Key Takeaways in 2025

Cocoa volatility has been the defining story of 2025, with prices soaring to historic highs before partially retracing. Despite ongoing commodity fluctuations, the bakery ingredients sector continues to exhibit steady overall growth, ranging between 4% and 7.6% annually across different forecasts. Innovation in clean-label, functional, and plant-based systems remains central to differentiation, while effective risk management through diverse sourcing and forward contracting is now essential. Regional variations in supply, such as those affecting eggs and fruit, underline the importance of localized strategies and supply resilience.

Strategic Recommendations for 2026

Agility in formulation will be critical, allowing manufacturers to substitute or rebalance ingredient blends in response to cost and supply shifts. Strengthening supplier relationships through long-term contracts or partnerships will enhance quality assurance and reduce volatility. Increased investment in R&D will support the development of functional plant proteins, enzyme systems, and novel fats and starches tailored to pastry and bakery requirements. Sustainability will continue to move from differentiation to expectation, with traceable, deforestation-free, and regenerative inputs becoming baseline standards. Data-driven procurement and regional dual-sourcing strategies will further mitigate risk.

Others Blog Articles…

Tags and Categories